By: Dr. Amelia Hart, CPA, and Steve Sledge, CPA

The Financial Accounting Standards Board (FASB) hit a significant milestone in 2023. Established in 1973, the FASB is still going strong, after 50 years. It continues to update, develop, improve, clarify and simplify accounting standards to provide users and capital market participants with decision-useful information.

Over the years, stakeholders have contributed to and been impacted by the FASB’s due process approach to identifying topics and conducting post-implementation reviews that seek to address issues that became known post-implementation.

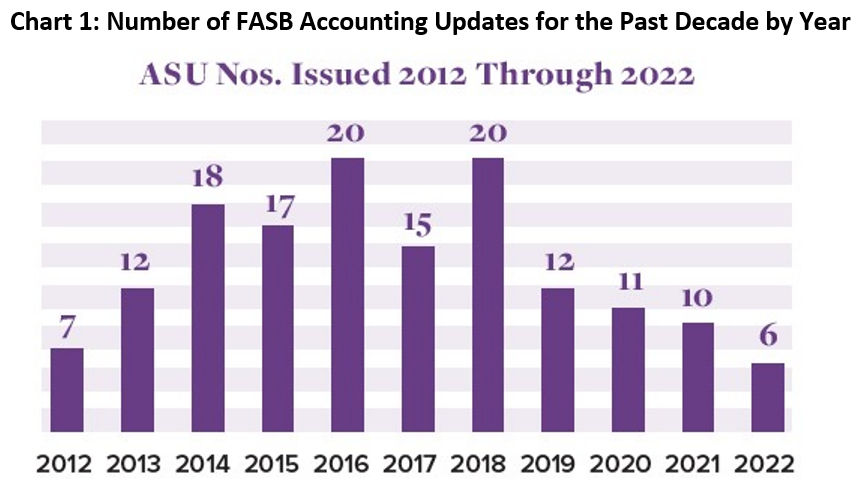

Over the past decade, the FASB has released significant updates on major topics. There was a noticeable increase in Accounting Standards Updates (Updates) in 2014, from seven Updates issued in 2012 to 18 in 2014 (see Chart 1). Significant issues such as business combinations, consolidations, intangibles, derivatives and hedges, revenue contracts with customers, financial instruments, stock compensation, not-for-profits, leases, and current expected credit losses have been addressed. The number of updates peaked at 20 Updates in 2016 and 2018 and is currently on a downward slope, with just six issued in 2022 (see Chart 1).

The FASB’s current technical agenda is informed by feedback from stakeholders in a 2021 Invitation to Comment (ITC). The results of the ITC were captured in a report that was released during June 2022.1 The FASB confirmed that the top seven most-cited issues are either on the agenda or being researched. The FASB continues to address issues that are of concern to its stakeholders.

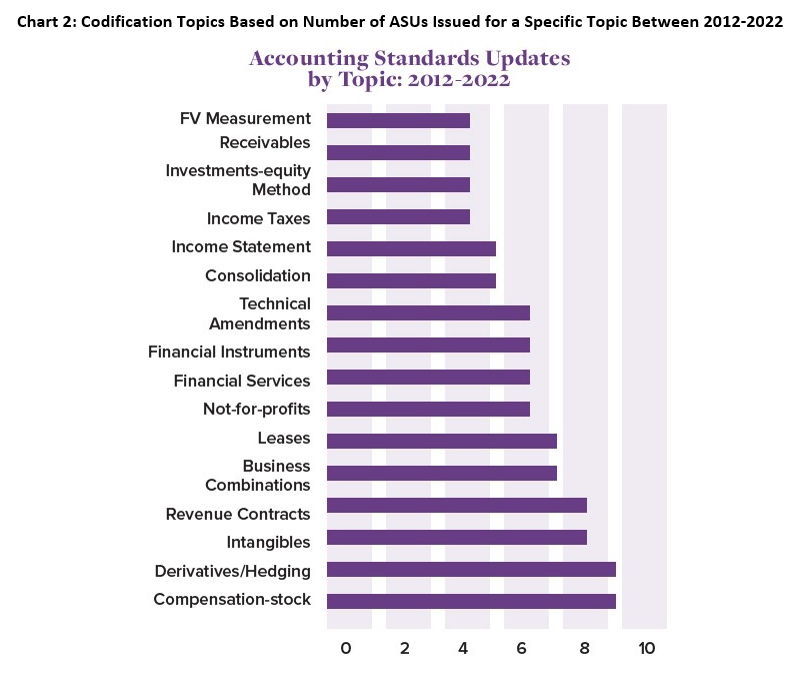

The significance of generally accepted accounting principles in our reporting environment is undeniable. We recognize the contributions of the FASB as a foundation of standard setting at its 50-year milestone. The following chart provides a reflection of the key accounting and disclosure areas impacted by the FASB’s standard setting over the past decade (see Chart 2).

Recent Accounting Standard Updates (Updates): Midyear 2023

As of June 30, 2023, the FASB released three Updates during 2023:

ASU No. 2023-01, Leases (Topic 842): Common Control Arrangements, addresses two issues based on its post-implementation review process. Issue 1 provides a practical expedient for private companies and not-for-profit entities that are not conduit obligors to refer to the written terms and conditions of a common control arrangement without regard to their legal enforceability. Issue 2 gives the requirements for accounting for leasehold improvements associated with common control leases between two entities. In general, all lessees (public or private) will amortize leasehold improvements related to a common control lease over their “useful life” to the common control group, regardless of the “lease term.” The Update is effective for fiscal years beginning after Dec. 15, 2023, including interim periods within those fiscal years. Early adoption is permitted for both interim and annual financial statements that have not yet been made available for issuance. If an entity adopts the amendments in an interim period, it must adopt them as of the beginning of the fiscal year that includes that interim period.

ASU No. 2023-02, Investments–Equity Method and Joint Ventures (Topic 323): Accounting for Investments in Tax Credit Structures Using the Proportional Amortization Method (A Consensus of the Emerging Issues Task Force), expands the accounting options for certain investments by expanding the use of the proportional amortization method. It allows reporting entities to elect to account for their tax equity investments using the proportional amortization method on a tax credit program-by-program basis if certain criteria are met. The ASU requires disclosures on an interim and annual basis for tax equity investments within tax credit programs for which the proportional amortization method is elected, regardless of if the proportional amortization method is applied. The Update specifies that this guidance becomes effective for public business entities for fiscal years beginning after Dec. 15, 2023, including interim periods within those fiscal years. For all other entities, the amendments are effective for fiscal years beginning after Dec. 15, 2024, including interim periods within those fiscal years. Early adoption is permitted, and amendments must be applied on either a modified retrospective or a retrospective basis.

ASU 2023-03 was issued to amend certain SEC paragraphs contained in the Accounting Standards Codification based on SEC bulletins and other communications.2

FASB Agenda for Second Half of 2023

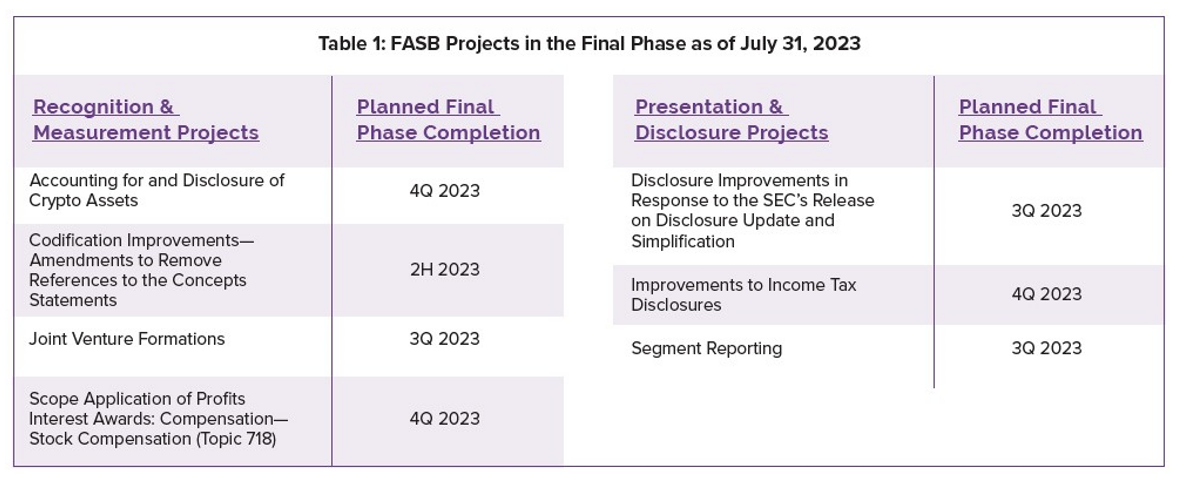

For the second half of 2023, the FASB agenda indicates that there are currently seven projects in the final phase (see Table 1).3

Planning for Fiscal Year-end 2023 Effective Dates

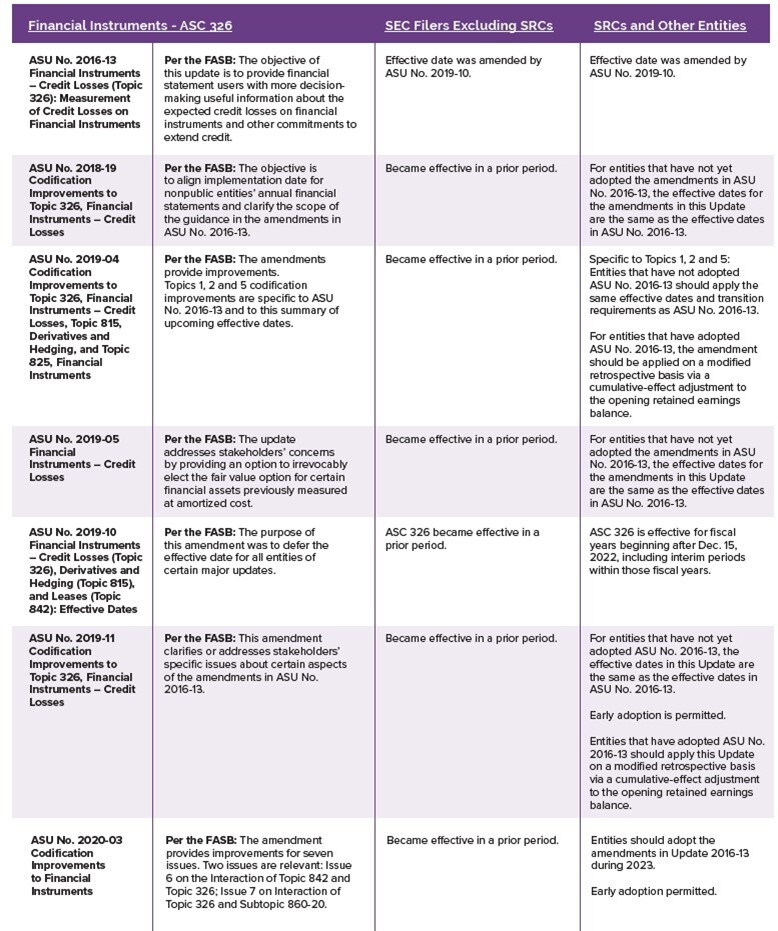

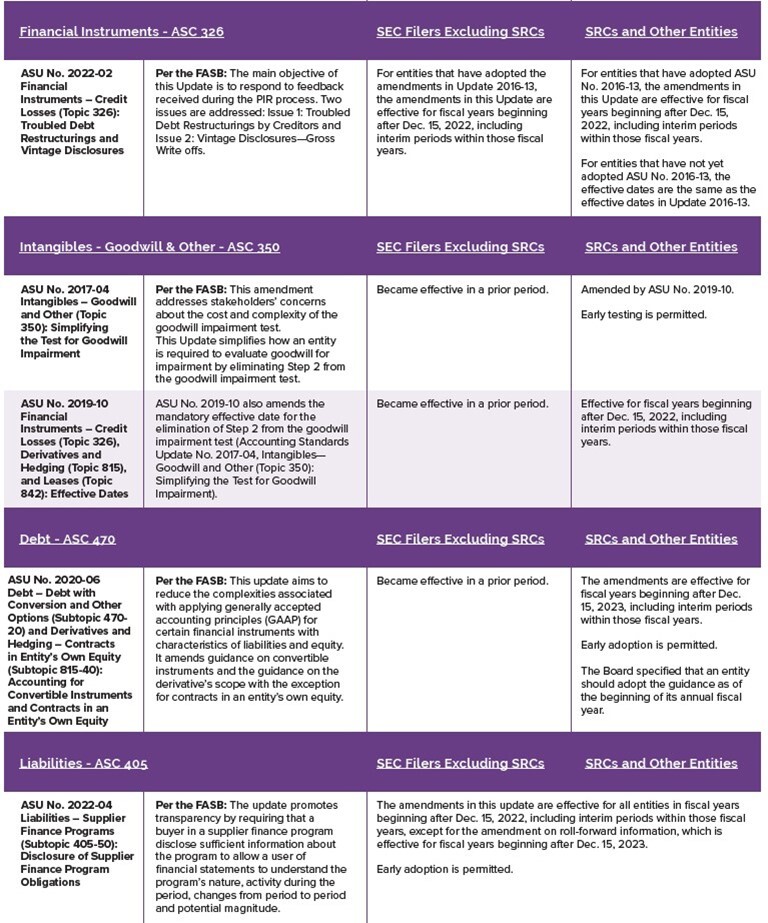

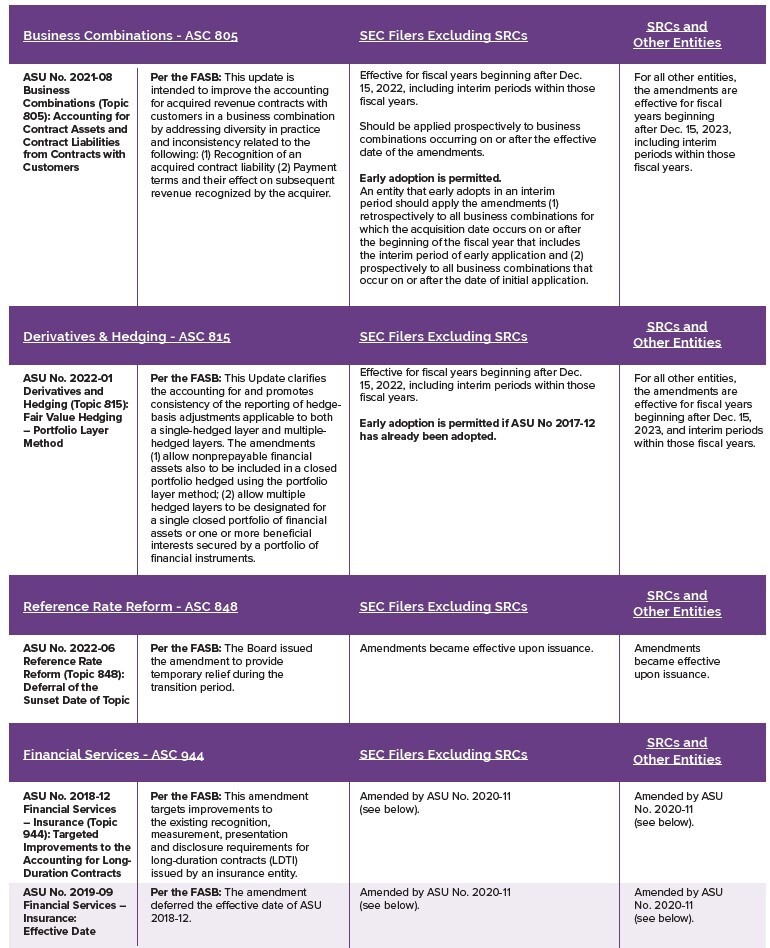

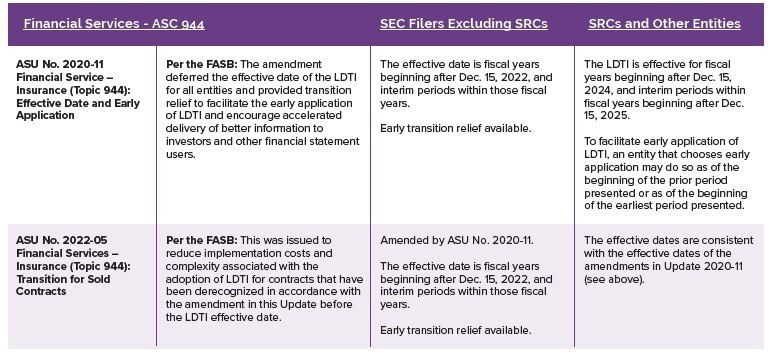

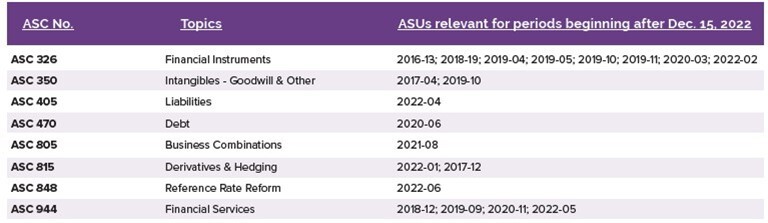

There are key Accounting Standard Updates (Updates) with implementation dates that become effective for periods beginning after Dec. 15, 2022, i.e., during calendar year 2023. This article provides a reminder of the Updates that will go into effect for public business entities (PBEs), smaller reporting companies (SRCs) and other entities.

The following summary of Updates does not provide the full scope of the guidance or transition guidelines as provided by the FASB in the respective Update releases. Information has been summarized with effective dates and includes the objective of each Update as indicated on the FASB website.4 The FASB effective dates apply differently to public business entities (PBEs) that are SEC filers, smaller reporting companies (SRCs) and other entities in alignment with the FASB’s staggering of effective dates between larger public business entities and other entities. Accordingly, the implementation dates will differ and should be considered in context with the type of entity that is applying U.S. GAAP.

The table reflects the updates by Accounting Standards Codification topic with the respective Updates shown below in date order. The objective descriptions are taken directly from the Updates. This summary provides an overview and should be considered in tandem with the full Update for the full scope of the guidance.5

Accounting Standards Updates Presented by Codification Topic for Calendar Year 2023

The Updates described above provide updates to the Accounting Standard Codification (ASC) as follows:

The Updates as discussed and corresponding matrix of the ASU’s amendments to the respective ASC as discussed above provide reminders of the current new requirements of the respective ASUs. Users should consult the actual Updates and related guidance and interpretations and consider consultation with qualified practitioners for specific impacts and considerations.

Additionally, a summary of professional standards and the related effective dates is also available at KPMG LLP’s Financial Reporting Review: http://bit.ly/3sbXFsK.

References

1See the full 2021 FASB Agenda Consultation Report available at http://bit. ly/3KH5gpv

2Accounting Standards Update 2023-03 – Presentation of Financial Statements (Topic 205), Income Statement - Reporting Comprehensive Income (Topic 220), Distinguishing Liabilities from Equity (Topic 480), Equity (Topic 505), and Compensation – Stock Compensation (Topic 718): Amendments to SEC Paragraphs Pursuant to SEC Staff Accounting Bulletin No. 120, SEC Staff Announcement at the March 24, 2022 EITF Meeting, and Staff Accounting Bulletin Topic 6.B, Accounting Series Release 280 - General Revision of Regulation S-X: Income or Loss Applicable to Common Stock (SEC Update). Available at http://bit. ly/3skFqRF

3FASB Technical Agenda with all project status is available at https://www. fasb.org/technicalagenda

4The Accounting Standard Updates and effective dates are available on the FASB website https://www.fasb.org/.

5The FASB effective dates and full Update is available at http://bit. ly/3qy6UD2

About the Authors

Dr. Amelia Hart, CPA, serves on the faculty of the Haslam College of Business in the Department of Accounting and Information Management at the University of Tennessee, Knoxville. She can be reached at ihart@utk.edu.

Steve Sledge, CPA, is a partner at KPMG LLP in Nashville. He can be reached at ssledge@kpmg.com.

This article was originally published in the September/October 2023 Tennessee CPA Journal.