By: Dr. Amelia Hart, CPA, and Steve Sledge, CPA

As practitioners and clients turn the corner from busy season and begin planning and risk assessment in the coming months, now is a good time for a refresher on recently promulgated updates as well as current Financial Accounting Standards Board (FASB) exposure drafts and projects with exposure drafts expected soon for future planning implications.

Recent Accounting Standards Updates (“Updates” or “ASUs”): Midyear 2024

The FASB released one Accounting Standards Update (Update) during 2024 (as of May 31, 2024) in addition to ASU 2024-02, Codification improvements – Amendments, to remove references to the concepts statements.1

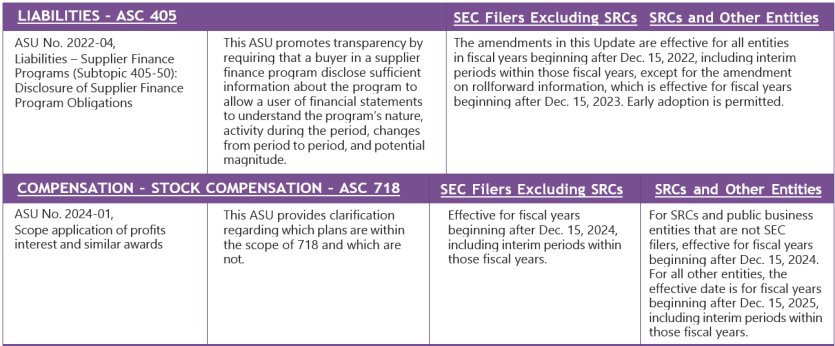

ASU No. 2024-01, Scope Application of Profits Interests and Similar Awards, under Compensation-Stock Compensation Topic 718, focuses on determining if a profits interest award should be accounted for as a share-based payment arrangement in accordance with ASC 718 or other compensation guidance. This determination requires judgment based on the facts and circumstances of the specific transaction. The ASU provides an illustrative example for this consideration, which includes four fact patterns that demonstrate the application of the scope guidance in paragraph 718-10-15-3. The intent of the ASU is to reduce complexity and diversity in practice related to the accounting for profits interest awards.2 See effective dates in the “effective dates” table below.

Although ASU No. 2024-01 will become effective for annual periods beginning after Dec. 15, 2024, the runway to adoption provides time for practitioners and companies to assess the guidance and consider the accounting implications on current or future profits interest awards.

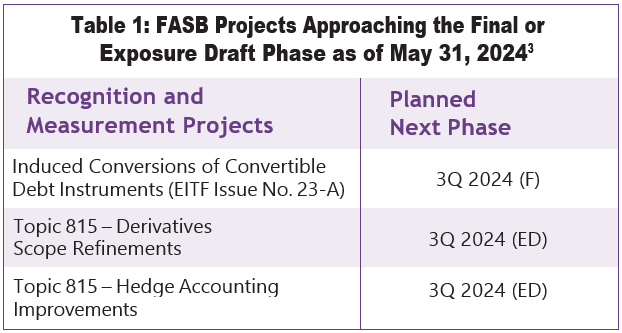

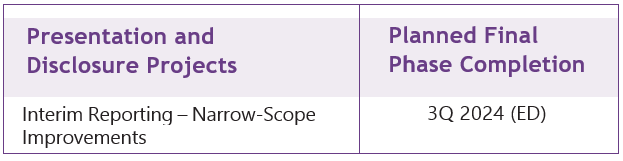

FASB Agenda for Second Half of 2024

For the second half of 2024, the FASB agenda indicates that there is one project approaching the final ASU (F) stage and five approaching the exposure draft stage (ED).

Planning for Fiscal Year 2024 Effective Dates (and Beyond)

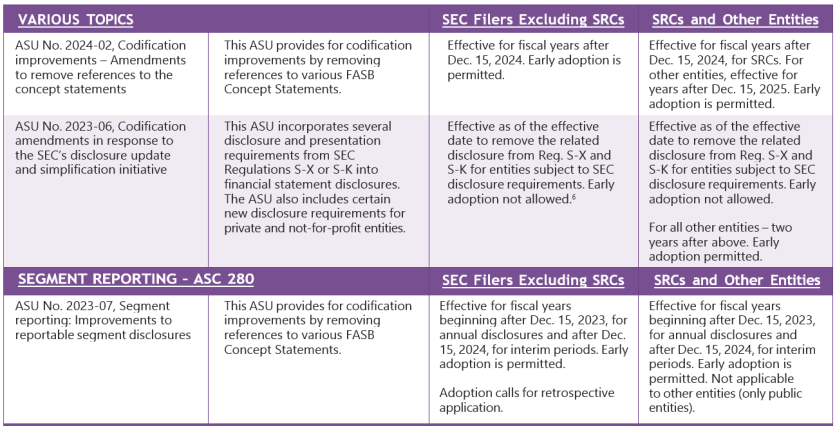

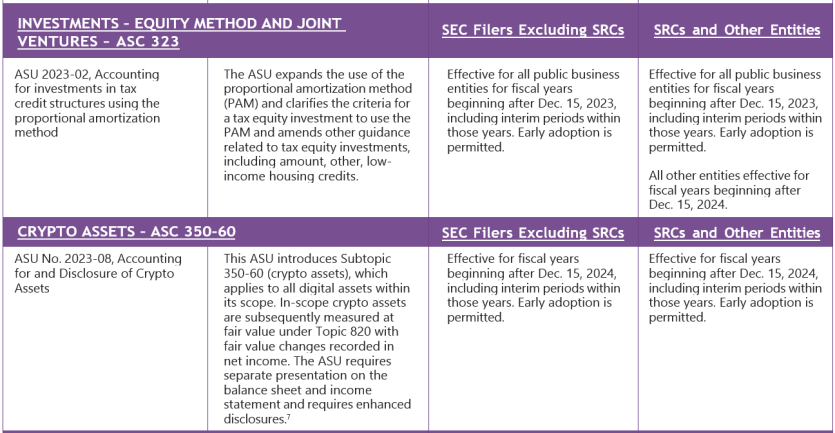

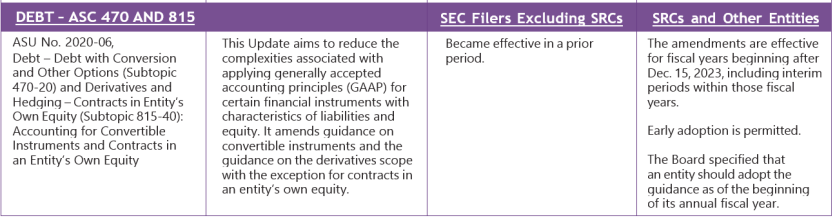

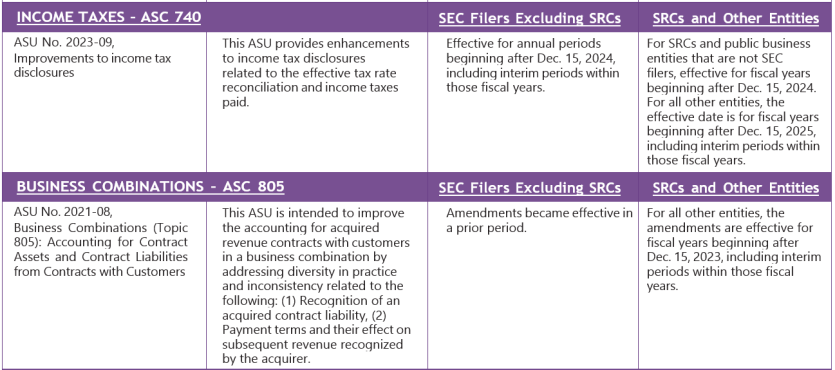

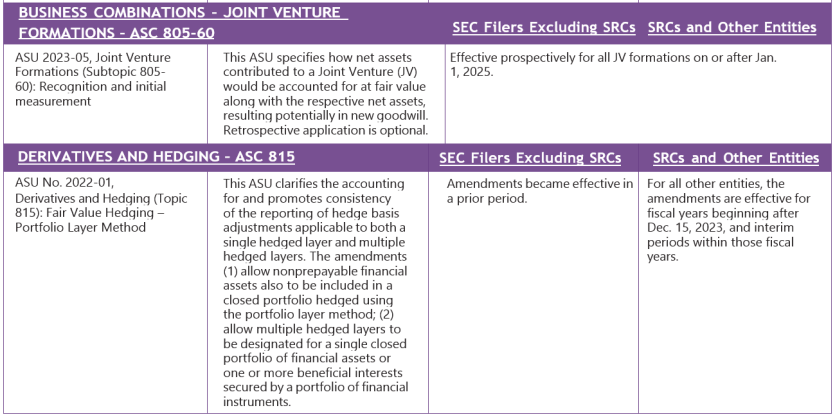

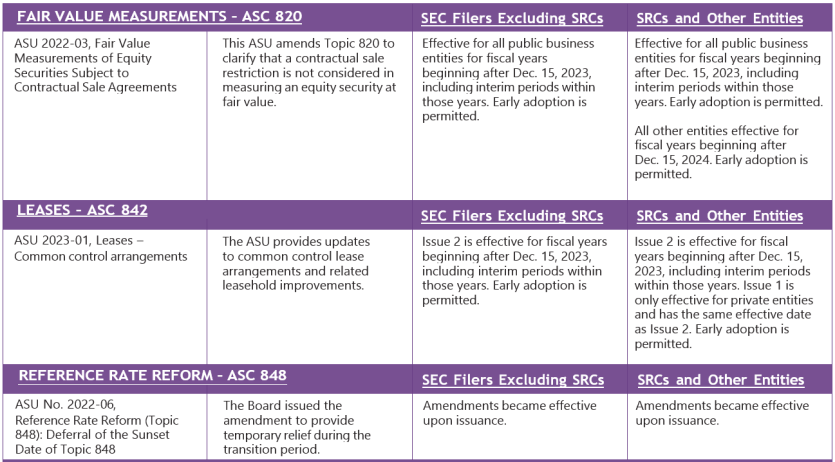

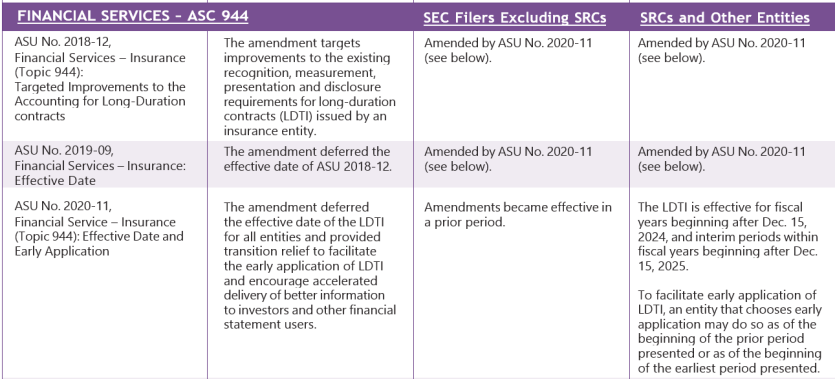

There are Accounting Standards Updates (Updates) with implementation dates that become effective for periods beginning after Dec. 15, 2023, i.e., during calendar year 2024. The table on the following page provides a reminder of the updates that will go into effect for public business entities (PBEs), smaller reporting companies (SRCs), and other entities in 2024 and subsequent periods.

The following summary of Updates does not provide the full scope of the guidance or transition guidelines as provided by the FASB in the respective Update releases. Information has been summarized with effective dates and includes the objective of each Update as indicated on the FASB website.4 The FASB effective dates often apply differently to PBEs that are SEC filers, SRCs and other entities in alignment with the FASB’s staggering of effective dates.

The table below reflects the updates by Accounting Standards Codification Topic with the respective Updates shown below in date order within each topic area. This summary provides an overview and should be considered in tandem with the full Update for the full scope of the guidance.

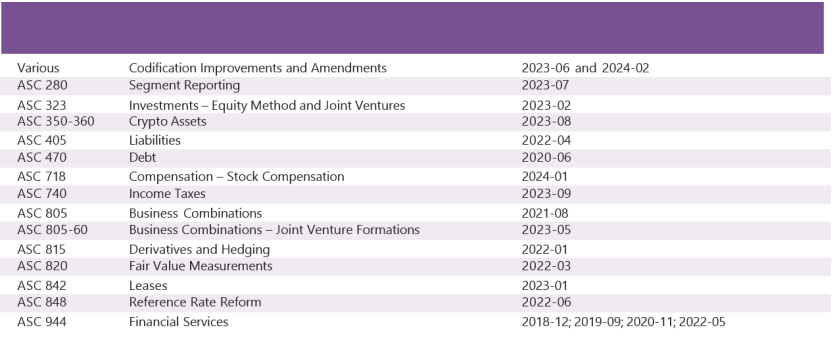

Accounting Standards Updates Presented by Codification Topic for Calendar Year 2023

The Updates described above provide updates to the Accounting Standard Codification (ASC) as follows:

The ASU effective dates and corresponding matrix of the ASUs’ amendments to the respective ASC as discussed above provide reminders of the current new requirements of the respective ASUs.

Users should consult the actual Updates and related guidance and interpretations and consider consultation with qualified practitioners for specific impacts and considerations. Additionally, a summary of professional standards and the related effective dates is also available at KPMG LLP’s Financial Reporting View “Accounting standards effective dates” (kpmg.com).

About the Authors

Dr. Amelia Hart, CPA, serves on the faculty of the Haslam College of Business in the Department of Accounting and Information Management at the University of Tennessee, Knoxville. She can be reached at ihart@utk.edu.

Steve Sledge, CPA, is a partner at KPMG LLP in Nashville. He can be reached at ssledge@kpmg.com.

References

1ACCOUNTING STANDARDS UPDATE 2024-02—Codification Improvements—Amendments to Remove References to the Concepts Statements (fasb.org)

2ACCOUNTING STANDARDS UPDATE 2024-01—Compensation—Stock Compensation (Topic 718): Scope Application o (fasb.org)

3See current projects of the FASB at FASB.org Current Projects (fasb.org)

4On June 4, 2024, the FASB directed staff to proceed with an ED for Accounting for Government Grants. The ED is expected in 3Q 2024.

5The Accounting Standard Updates and effective dates are available on the FASB website (fasb.org)

6If by June 30, 2027, the Securities Exchange Commission (SEC) has not removed the existing disclosure requirement from Regulation S-X or S-K, the corresponding disclosure pending requirements will be removed from the Accounting Standards Codification (ASC) and would not become effective for any entities.

This article was originally published in the July/August 2024 Tennessee CPA Journal.