By: Joel Busch, CPA, JD, MST

When it comes to the reasons behind a charitable donation by a business, the non-tax drivers normally take center stage – from the altruistic goals of the company to the potential public relations benefits it affords them. However, the tax benefits of a donation by a business often will have a significant impact on how and when a particular contribution is made. While cash donations are the norm for many companies, for those who decide to make non-cash donations, a common issue is which type of asset should be donated to a particular charity. While tangible assets (such as inventory or real estate) are commonly donated, intangible assets can be and are donated to charities as well.

Separate from other types of intangible assets, such as stocks and other securities, the Code contains a special set of rules, including the potential for a “bonus” additional deduction, for taxpayers who donate a very specific type of intangible asset, referred to as qualified intellectual property (QIP) in the Code.1

This paper will cover what assets can qualify as QIP, the special requirements imposed on a donor and donee of QIP, the potential federal tax benefits to the donor of QIP, and

real-life examples of when donations of QIP can provide more benefits than other forms of donations – all with a primary focus on C corporations (noting that the QIP rules apply to donors beyond C corporations).

What Are Qualified Intellectual Property Assets?

Not all intellectual property is considered “qualified intellectual property” under federal law. IRC §§170(m)(9) and 170(e)(1) (B)(iii) mutually define QIP to include any of the following assets:

• Patents

• Copyrights2

• Trademarks

• Trade names

• Trade secrets

• Know-how

• Most software which is not generally available for purchase by the public

The Initial Deduction for Donations of QIP

The initial deduction for a corporation on a donation of QIP, subject to annual deduction limitations based on modified taxable income, is the lesser of the QIP’s fair market value or the taxpayer’s basis in the QIP at the time of the contribution.3 Therefore, a taxpayer contemplating this type of contribution will first need to make sure they properly ascertain the asset’s adjusted basis at the time of the planned contribution, keeping in mind that if it is subject to amortization, if for some reason the adjusted basis should have been lower than the amount the donor has on its tax amortization schedules (due to, say, a prior year miscalculation), the lower (correct) basis must be used as the deduction limitation amount (if less than the fair market value).4 Then the fair market value of the QIP must be properly determined as well, with the likely need for an appraisal.

The Role of the Appraisal

Like most other non-cash donations, the fair market value of a contributed asset must be determined in order to determine the potential allowable initial deduction for the donor. As such, a proper appraisal should be used by the donor of QIP, utilizing an appraiser that is properly qualified and knowledgeable on the specific type of contributed QIP.

However, one compliance break for actual QIP donations is that even if the deduction is more than $5,000, unlike most other non-cash donations, QIPs are exempt from the requirement to have a qualified appraisal (as defined in IRC §170(f)(11)(E)) attached to the tax return.5

The “Bonus” Additional Post-Contribution Deduction

If the donor of QIP gives the required notice (discussed later) to the charity that they are making a donation of qualified intellectual property, then in addition to the initial charitable deduction based on the lower of the QIP’s basis or fair market value as discussed above, the donor is also able to potentially claim an additional deduction based on a percentage of the amount of net income the charitable organization realizes from the donated QIP after they obtain ownership of it from the donor.6

This additional deduction for the donor has a number of rules and complexities, with the primary ones being:

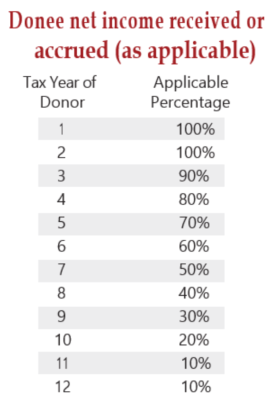

1. A percentage (the “applicable percentage”) is applied every year to the amount of donee net income that is generated from the QIP that is then used in the calculation for the potential additional deduction for the donor. However, the applicable percentage is not a flat percentage, but rather a series of annual rate percentages that go down over time.7

The following table contains the applicable percentage of donee net income used in the calculation of the additional charitable deduction for the donor of QIP:

Note #1: The donee’s tax year is used to capture the amount of net income generated by the donee on donated QIP every year before applying the applicable percentage, and the last day of the donee’s tax year is used to determine which tax year applicable percentage is used on the table. Net income generated by a charity for the period of July 1, 2023, to June 30, 2024, on a donation of QIP made on Aug. 1, 2023, the applicable percentage for year two of the table would be used, if the donor uses a calendar year and the donee uses a June 30 fiscal year-end.

Note #2: There is no clear guidance on what constitutes donee “net income” attributable to QIP. IRC §§6050L(d)(1)(D) and 170(m)(10)(B) both refer to each other and simply state that the additional deduction calculated is based, in part, on the “net income determined by donee.” There is no other IRS or other legal guidance on what exactly gets included in the donee net income calculation, so a reasonable conclusion could be for the charity to subtract any expenses directly related to the QIP against its gross income from the QIP in order to report the proper amount of net income to the donor.

2. The additional deduction only kicks in for the donor when the cumulative net income of the donee from the QIP, after applying the year-based percentages using the table above, exceeds the initial deduction amount for the donor, as detailed earlier.

Example

On Oct. 16, 2024, Acme Corporation, which uses a calendar year, donates a patent, which is QIP, to a qualified calendar-year charity. Acme makes the required notice to the charity that it is making a donation of QIP at the time of the contribution. The basis of the patent to Acme is $100,000, and its fair market value is $225,000.

So, the initial contribution deduction (subject to the overall 10% of adjusted taxable income limitation) for Acme is $100,000 (as the basis of the patent was lower than the fair market value). After the transfer, the charity licenses out the patent to outsiders, and its net income from the patent is $3,000 in 2024 and $50,000 each year from 2024 through 2030.

Using the net income percentage table above, the applicable amounts used to determine if the cumulative additional deduction threshold for Acme has been met are as follows:

$3,000 for 2024 (100% of $3,000)

$50,000 for 2025 (100% of $50,000)

$45,000 for 2026 (90% of $50,000)

$40,000 for 2027 (80% of $50,000)

$35,000 for 2028 (70% of $50,000)

$30,000 for 2029 (60% of $50,000)

$25,000 for 2030 (50% of $50,000)

Therefore, no additional deduction would be applicable to Acme for the years 2024 through 2026 as the cumulative amount through 2026 is only $98,000, which is less than the $100,000 initial deduction based on the patent’s basis at the time of the contribution.

However, for 2027, Acme is now eligible for a $38,000 additional deduction (the first $2,000 of the $40,000 figure above gets them to the $100,000 additional deduction threshold). Acme’s additional deduction for the years 2028, 2029 and 2030 would be $35,000, $30,000, and $25,000.

3. The additional deduction period for the donor ends for any income the charity may receive (or accrue, if applicable) after the 10-year period beginning on the date of the contribution.8 The reason for the 12-year period in the applicable percentage table above is for situations where the donor and donee may have different tax years and for short tax years.

4. The additional charitable deduction is not allowed to a donor on contributions to most private foundations.9

5. In order to potentially take advantage of the QIP rules, a donor must, at the time of the contribution, inform the charity that they intend to treat the donation as a QIP donation.10

There is no formal form for this notice, but IRS Notice 2005-41 provides guidance on this important requirement. The donor can either mail or deliver the following information to the charity to fulfill this notice requirement:

1. The name, address and taxpayer identification number of the donor;

2. A description of the qualified intellectual property in sufficient detail to identify the qualified intellectual property received by the donee;

3. The date of the contribution to the donee; and

4. A statement that the donor intends to treat the contribution as a qualified intellectual property contribution.

Annual Information Returns by Charities to Donors and the IRS

Charitable organizations who receive a QIP donation must normally report their applicable net income from the QIP every year, along with other basic information on the charity, the donor and the type of QIP included in the report, by the end of the month following the donee’s tax year to the donor as well as to the IRS. This is done via IRS Form 8899.11 Form 8899 is not required in years in which the donee does not generate any net income or for a tax year that starts more than 10 years after the contribution. In addition, any net income generated by the donee after the legal life of the QIP is not reported on Form 8899, as well as any post-legal life of the QIP income received by the charity is not eligible towards the additional deduction by the donor.12

Reasons for Donating QIP Instead of Cash or Other Assets

For those taxpayers who have QIP that they can potentially donate, when deciding whether they should donate QIP or make another type of donation instead, there are certain situations where the donation of QIP could be a prudent choice for federal tax purposes. The following are two situations where a QIP donation could be the way to go for the business.

1. Upcoming Expected Tax Losses Coupled and Expiration of Prior-Year Excess Charitable Contribution Carryovers

A QIP donation can be a very valuable tax planning tool when a taxpayer has an excess charitable contribution from a prior year, especially when tax losses are predicted in upcoming tax years. Under IRC §170(d)(2)(A), if a corporate taxpayer makes charitable contributions over a certain amount for the year, the excess contribution can be carried over for up to five years, after which time, any remaining excess contribution expires. For C corporations, for most contributions, the annual charitable contribution limit is 10% of modified taxable income.13 When the excess contribution is carried over into the subsequent year, the total allowable contribution deduction in that subsequent year takes into account not only any excess charitable contribution carryovers but also the actual contributions made in the current year. However, if the total amount of the carryover and current-year contributions exceeds the annual deduction limit for the year (i.e., the 10% of adjusted taxable income), the current-year contributions must be used up first before any carryover contributions can be used.14 This excess contribution system can make it attractive for a business to make a QIP contribution when they have some contribution carryovers that are getting close to the five-year expiration period.

Example

Beta Corporation, a cash-basis, calendar-year C corporation, has a $100,000 excess charitable contribution carryover from the 2019 tax year. In 2024, it has $1.3 million of adjusted taxable income. Through November 2024, it has made $100,000 of cash charitable contributions. Its public relations department wants to make another $60,000 in contributions by the end of the year to fulfill a pledge it made to the public at the beginning of the year to donate at least $160,000 for the entire year.

At this point, the corporation is contemplating two options: making either a $60,000 cash donation or a QIP donation of a patent with a fair market value of $60,000 and an adjusted basis of $5,000. The corporation predicts that a charity could license out the patent and generate $83,000 of donee net income (after applying the applicable annual percentage amounts as discussed previously) in years six through eight after the contribution (2030 to 2032). Beta also predicts tax losses for the years 2025 through 2029.

If Beta goes with the cash donation, only $30,000 of the $60,000 cash donation can be deducted on its 2024 tax return ($1.3 million of adjusted taxable income x 10%), given the

$100,000 in prior donations for the year. As a result, all of the 2019 charitable contribution carryover of $100,000 will be permanently lost as 2024 was the final carryover year for these particular contributions. Furthermore, if Beta does not generate any taxable income for the subsequent five years (2025 through 2029), all of the $30,000 excess charitable contribution from 2024 will be permanently lost as well.

On the other hand, if Beta goes with the QIP donation instead, then the initial basis of the patent of $5,000 (since it is less than the $60,000 fair market value) will be deductible on its 2024 return, and $25,000 of the 2019 tax-year contributions will also be deductible

in 2024, resulting in a total charitable contribution of $130,000 on its return for 2024 (the same as the earlier cash donation scenario).

However, assuming that the charity does in fact generate net income on the patent as predicted by Beta, after the first $5,000 of donee net income (as adjusted by the annual applicable percentage tables), all of the remaining $78,000 of adjusted donee net income generated in the years 2030 through 2032 will be deductible by the corporation, assuming Beta generates sufficient taxable income in those years.

In the two scenarios above (cash versus QIP), Beta is better off going with the QIP donation as it will receive a total of $208,000 in charitable deductions from 2024 through 2032, whereas it will generate only $130,000 of charitable deductions with the cash donation.

2. Anticipating Higher Federal Marginal Tax Rates in Future Tax Years

A donation of QIP by a business may also be more attractive than a cash or non-QIP property donation if they anticipate being eligible for the additional QIP deduction and the owner(s) of a non-C corporation business expect to be in a higher tax rate bracket in future years.

Example

Productions LLC, a single-member LLC owned by Noriko Jones, is contemplating making a donation of QIP to a qualified charity. It is contemplating giving either (1) cash of $10,000, (2) a tangible asset with a fair market value of $10,000 and a basis of $23,000, or (3) a patent with a fair market value of $10,000 and a basis of $8,700.

In the current tax year, Noriko is in the 22% marginal tax bracket, but due to anticipated changes in her income, she expects to be in the 37% marginal bracket starting the following year and going into future tax years.

The cash and tangible property asset donations in the current year would each provide Noriko with a $2,200 federal tax savings for the year ($10,000 x 22%).

However, if the LLC were to make the QIP donation, because the adjusted basis in the patent is less than its fair market value, Noriko’s initial federal deduction would only be $8,700 – resulting in an initial contribution-year federal tax savings of $1,914 ($8,700 x 22%). If the patent ends up generating net income to the charity of $3,000 (adjusted by the applicable percentage amounts) for the next five years, then starting in the third year after the donation she would start to be able to claim the Section 170(m) additional deductions, which would be $300 in year three and $3,000 per year in years four and five. The $6,300 of additional deductions would result in a cumulative tax savings of $4,245 (the initial $1,914 tax savings in year one, plus the $2,331 ($6,300 x 37%) for years three through five), which results in more overall tax savings to Noriko than the cash or tangible property options, which gave her only $2,200 in total federal tax savings.

Conclusion

While not all businesses have qualified intellectual property that they can potentially contribute to a charity, for those that do, in certain situations the QIP donation can be a better option than donating cash or non-QIP assets. It is extremely important that a tax practitioner is aware of all of the requirements necessary in order for their client to potentially be eligible for the additional QIP deduction (including the important notice requirement) and to work closely with the client’s legal counsel who will be leading the non-tax aspects of the transfer of the qualified intellectual property to the charity.

About the Author

Joel Busch, CPA, JD, MST, is an associate professor at San Jose State University, where he teaches tax courses at both the graduate and undergraduate levels. Busch is a member of the American Accounting Association, the Institute for Professionals in Taxation, the California Society of Certified Public Accountants and the California Bar Association. He can be reached at joel.busch@sjsu.edu.

References

1 IRC §170(m)(1)

2 Only copyrights that are not self- created, or if acquired, where the initial basis of the buyer/transferee is the same as the seller/transferor.

3 IRC §170(e)(1)(B)

4 IRC §1016(a)(2)

5 IRC §170(f)(11)(A)(ii)(I)

6 IRC §170(m)

7 IRC §170(m)(7)

8 IRC §170(m)(5)

9 IRC §§170(m)(9) and 170(e)(1)(B)(ii)

10 IRC §170(m)(8)b)

11 IRC §6050L(b)(1)

12 Treas. Reg. §1.6050L-2(a)

13 IRC §§170(b)(2)(A) and 170(b)(2)(D)

14 IRC §170(d)(2)(A)

This article was originally published in the November/December 2024 Tennessee CPA Journal.