By: Dr. Amelia Hart, CPA, and Steve Sledge, CPA

On Sept. 12, 2024, the American Institute of CPAs (AICPA) and the National Association of State Boards of Accountancy (NASBA) jointly proposed a new initiative in the form of an Exposure Draft aimed at enhancing the pathways to Certified Public Accountant (CPA) licensure.1 This proposal, referred to as the CPA Competency-Based Experience Pathway, would provide an alternative option for candidates to fulfill the CPA licensure requirements. There would be no additional coursework or master’s degree beyond the bachelor’s degree after candidates complete a bachelor’s degree and meet a state’s licensure requirement of specific accounting and business courses.

This proposed Competency-Based Experience (CBE) Pathway is not just a must-read; it should be read multiple times, carefully considered by stakeholders, and responded to within the comment period. This proposal will undoubtedly shape and influence the profession in the future. Our hope in writing this article is that stakeholders will participate by lending their voices to the future of the profession.

One of the perceived challenges for the profession is the declining accounting majors and CPA candidates. The AICPA and NASBA aim to address this accounting pipeline issue and offer an alternate pathway for candidates who face other barriers to licensure. The proposal also aims to increase flexibility for CPA candidates, respond to evolving market conditions, and ensure the protection of the public interest. The proposal cites parties expected to be impacted, including CPA candidates, hiring organizations or individuals, persons overseeing a candidate’s work, and various boards of accountancy. It should be noted, however, that other stakeholders will also be impacted by the proposal.

We encourage broad stakeholder input. This article on the proposal does not seek to offer opinion or analysis; instead, we seek to encourage the active participation of readers.

The Competency-Based Experience (CBE) Pathway: Some Key Tenets

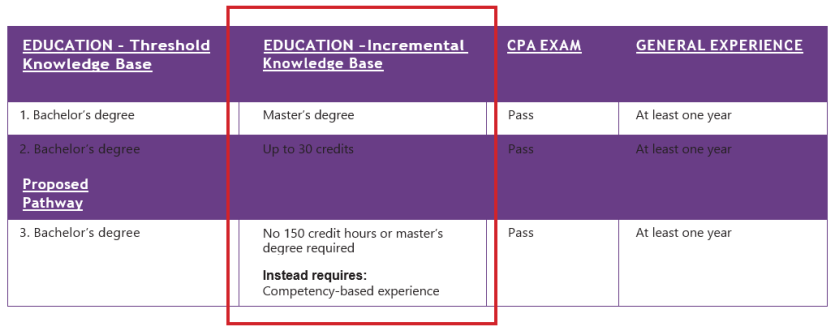

There are currently two pathways to obtaining a CPA license, both requiring specific educational requirements, passing the CPA Exam and gaining general experience. The bachelor’s degree was the initial education requirement. In 1988, the AICPA recommended that state accounting boards raise the education requirement to 150 credit hours. By the early 2000s, most states adopted the 150-hour (education) rule for CPA licensure, requiring candidates to complete 150 semester hours (or a master’s degree).

There have been widespread conversations on addressing pipeline issues, attracting new talent, and creating alternatives or modifications to address concerns about the cost, access, and accessibility of meeting the education requirements. The proposed CBE pathway would offer an alternative for candidates, marking a significant shift from current requirements. The diagram emphasizes two pathways and the proposed pathway.

The CBE Pathway Expanded

The pathway includes education, competency-based experience, general experience and CPA Exam requirements (plus ethics, if applicable by the state) for licensure. The proposal states that all requirements, except for education, should be completed in the order specified by the candidate’s board of accountancy. The proposal expounds on each of the items that are presented in summary form on the following page.

The 4 Components of the CBE Pathway

1. Education:

☐ Bachelor’s degree with required accounting and business courses.

2. Competency-Based Experience:

☐ To be completed under the supervision of a CPA evaluator.

☐ Acceptable experience includes employment or volunteer services in industry, government, academia or public practice.

☐ Duration: Minimum of one year and up to a maximum of five years, totaling at least 2,000 performance hours.

☐ Internship credit is not allowed for competency-based hours.

☐ Candidates work closely with their CPA evaluators.

☐ After completing at least one year of competency-based experience, the CPA evaluator may submit the competency-based experience form.

3. General Experience:

☐ One additional year of general experience as per current Uniform Accountancy Act (UAA) requirements.

☐ Any excess beyond one year and 2,000 hours from the competency-based performance can be applied to fulfill this requirement.

4. CPA Exam:

☐ Remains unchanged; passing the exam is mandatory.

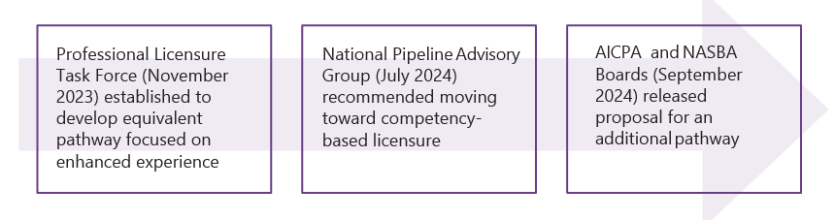

Diagram 2: The Development of the Proposed Pathway2

Competencies in the Context of the CBE

Competency is defined on page 7 of the proposal as “an identified set of knowledge, skills, abilities, and behaviors to be exhibited by a candidate” and is separated into two categories: Professional and Technical. The seven professional competencies and three technical competencies are detailed with the expected demonstrated characteristics in Appendix A of the proposal.

Competencies Identified in the CBE Pathway Proposal

Professional Competencies

- Ethical behavior

- Critical thinking and professional skepticism

- Communication

- Collaboration, teamwork and leadership

- Self-management and continuous learning

- Business acumen

- Technology mindset

Technical Competencies: Specific to accountancy and classified into three categories

- Audit and assurance

- Taxation

- Business and financial reporting

Candidates would need to complete 2,000 hours of relevant technical experience within a five-year period and would be eligible to apply for the pathway after one year of experience and having completed the 2,000 hours. One or more CPA evaluators3 (often employed by the same entity as the applicant)4 would evaluate and assert whether the applicant exhibits the professional competencies and at least one of the three technical competencies, which would be verified by one or more evaluators in their organization. The professional competencies include critical thinking, problem solving and communication, while the technical competencies focus on audit and assurance, tax, and advisory services. Candidates pursuing this pathway would also have to complete a separate year of general experience and pass the CPA Exam.

In Review: What Are the Potential Impacts and Benefits?

Stakeholders should weigh the potential impacts and benefits. Several examples are noted below.

1. Increasing accessibility and flexibility

One goal of the CPA Competency-Based Experience Pathway is to increase accessibility and flexibility for CPA candidates. Unlike the traditional requirement to complete 150 hours of college-level credits,5 this pathway allows candidates who may not have access to such opportunities to demonstrate their skills and knowledge through a more flexible framework. Will this increase the flow of new talent?

2. Valuing competency-based experience

The proposal explores a pathway to certification that does not require 150 credit hours. Stakeholders might consider whether the benefit of this alternate pathway complements market needs and reflects the added value of the professional.

3. Aligning with market needs

The proposal aims to align the CPA licensure process with current market needs, a growing demand for professionals with a broad range of skills and competencies. The pathway would provide an alternative way for CPA applicants to obtain the respective licensure requirements that complement market needs.

In Review: Challenges and Considerations

Stakeholders should weigh the challenges and considerations. Several examples are noted below.

1. Consistency, fairness and risk in evaluating competencies

One potential challenge is ensuring consistency and fairness in the evaluation of competencies. The proposal requires competencies to be verified by licensed CPAs in the workplace, which could lead to variations in the assessment process.

2. Implementation and logistical challenges

The introduction of a new pathway may necessitate adjustments to current state-level requirements, processes and systems, which could present logistical challenges.

3. Varied concerns on process and CBE evaluation

Additional challenges may be introduced related to quality assurance, conflict of self-interest by CPA evaluators, verification challenges, resistance by current license-holders and equity issues.

Comments and Comment Period: Stakeholder Engagement and Feedback

The open comment period for the proposal is a critical aspect of its development. By inviting feedback from a wide range of stakeholders, including CPA candidates, educators, employers and regulators, the AICPA and NASBA are ensuring that the final framework is comprehensive and effective. This collaborative approach allows for the incorporation of diverse perspectives and insights, ultimately leading to a more robust and well-rounded pathway. Stakeholder engagement is essential for creating a licensure process that meets the needs of the profession and the public.

The proposal invites feedback through Dec. 6, 2024. This open comment period allows stakeholders to provide their insights and suggestions, ensuring that the final framework is comprehensive and effective in meeting the needs of the profession. Instructions for providing comments are included in the proposal, which can be found on the AICPA website.

Conclusion

The AICPA’s and NASBA’s proposal in the form of an Exposure Draft for the CPA Competency-Based Experience Pathway provides an alternative pathway to licensure that could help address the evolving needs of the accounting profession. This article is intended to summarize the proposal, and the authors encourage constituents to respond to the invitation for comments in order to contribute to the consideration of the input from the broader profession.

References

1 The Exposure Draft, CPA Competency-Based Experience Pathway issued September 12, 2024 is retrievable at https://bit.ly/cbedraft

2 See page 1 of the Exposure Draft, CPA Competency-Based Experience Pathway issued September 12, 2024, retrievable at https://bit.ly/cbedraft

3 Competencies would be verified in the workplace by licensed CPAs.

4 Note that the proposal includes discussion of completing the evaluation in circumstances where the applicant’s organization does not have a CPA to serve as evaluator or when an applicant changes employers and similar situations.

5 This requirement is often fulfilled by obtaining a master’s degree or completing a double major of undergraduate studies that meet certain state-specific course requirements for eligibility.

About the Authors

Dr. Amelia Hart, CPA, serves on the faculty of the Haslam College of Business in the Department of Accounting and Information Management at the University of Tennessee, Knoxville. She can be reached at ihart@utk.edu.

Steve Sledge, CPA, is a retired KPMG LLP partner. He can be reached at sdsledge@outlook.com.

This article was originally published in the November/December 2024 Tennessee CPA Journal.