By: Dr. Amelia Hart, CPA, and Steve Sledge, CPA

Building on the preceding article,1 we suggest in this article that periods of uncertainty should not be immediately overwhelmed with efforts to provide answers, but rather, they should be met with questions. Taking time to ask questions is a pathway to understanding a company’s or client’s unique context, making accounting and financial guidance more relevant, targeted and effective. Questions encourage trust, collaboration, ownership and participation in decisions about how to move forward.

In this article, we both encourage and suggest questions that may be asked during periods of uncertainty. The suggested questions are intended as prompts to guide more targeted inquiry by the reader and, as such, do not represent a comprehensive list of all possible questions during periods of uncertainty.

The Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) serves as the primary source of U.S. Generally Accepted Accounting Principles (GAAP) for non-governmental entities. It provides authoritative guidance to help professionals navigate periods of uncertainty and deliver decision-useful information to financial statement users. Our focus is on FASB guidelines relevant to entities that follow U.S. GAAP. Professionals applying statements from the Governmental Accounting Standards Board (GASB) or the International Financial Reporting Standards (IFRS) may still find the discussion applicable and insightful.

Why Ask Questions?

Accounting professionals are solution providers, whether providing general-purpose financial statements or offering assurance through an opinion. Asking questions during times of uncertainty is a vital part of that process, helping to thoughtfully assess a company’s situation in light of relevant technical accounting guidance.

Questions accomplish several objectives:

- They challenge us to consider perspectives we may have overlooked, using exploratory thinking to guide our approach.

- They encourage a process that leverages different voices of experience, expertise and perspective.

- They help uncover issues, clarify intent and build shared understanding, which could then become the basis for assessing risk during periods of uncertainty.

- They invite active listening. Listening is one of the most effective ways to diagnose problems, issues or concerns, and it fosters trust and credibility through a sense of shared purpose.

During periods of economic uncertainty, particularly when businesses are navigating many unknowns, asking the right questions becomes essential. Taking time to pause, reflect and engage others can lead to more effective decision-making. This process helps shape a clear path towards a plan of action and can be most helpful in getting to the right answer in the most efficient manner (e.g., timely, comprehensive, holistic).

Questions as a Compass

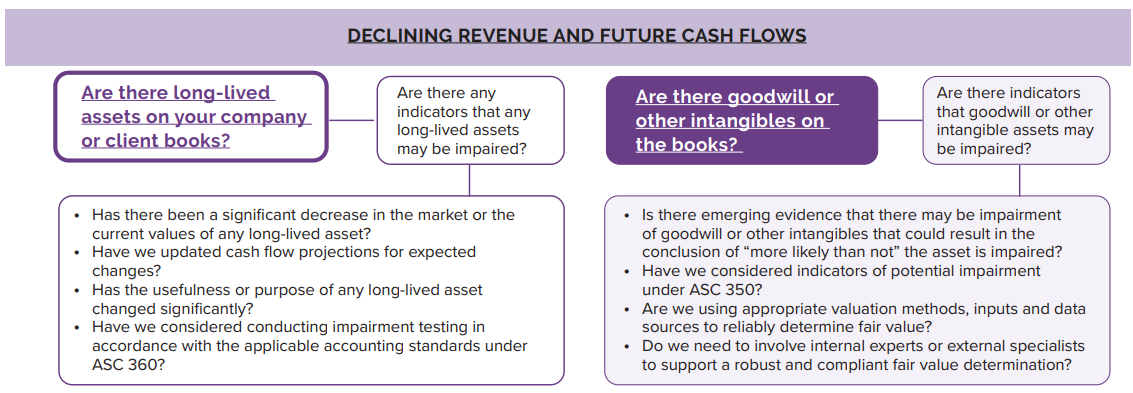

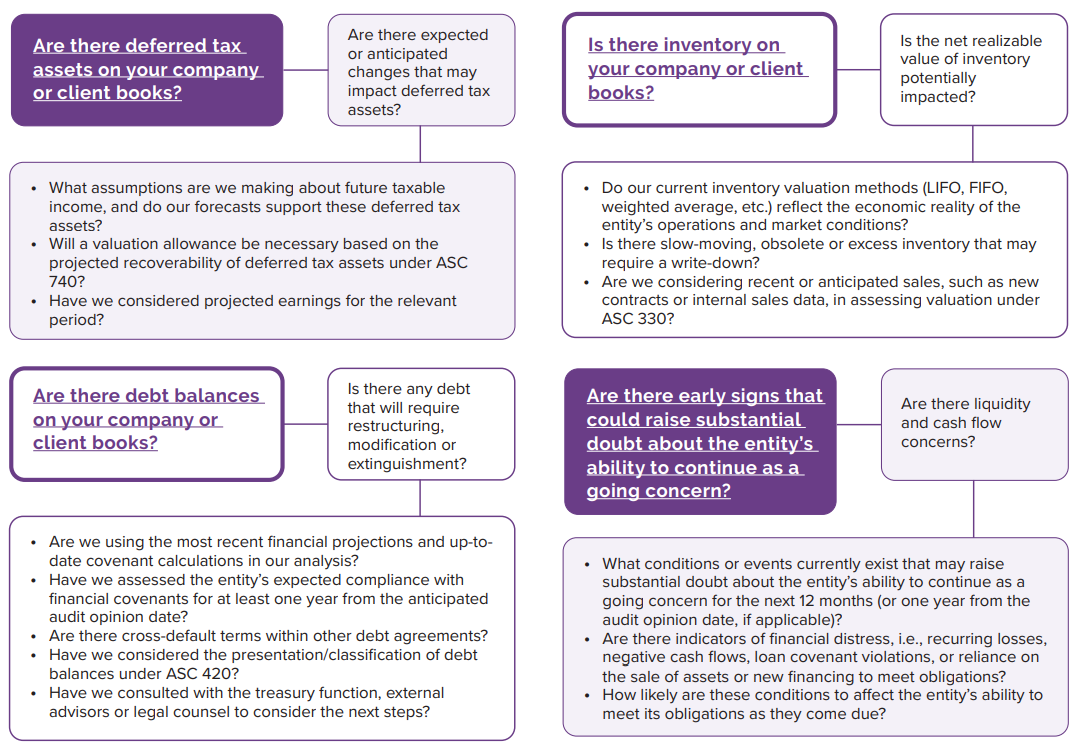

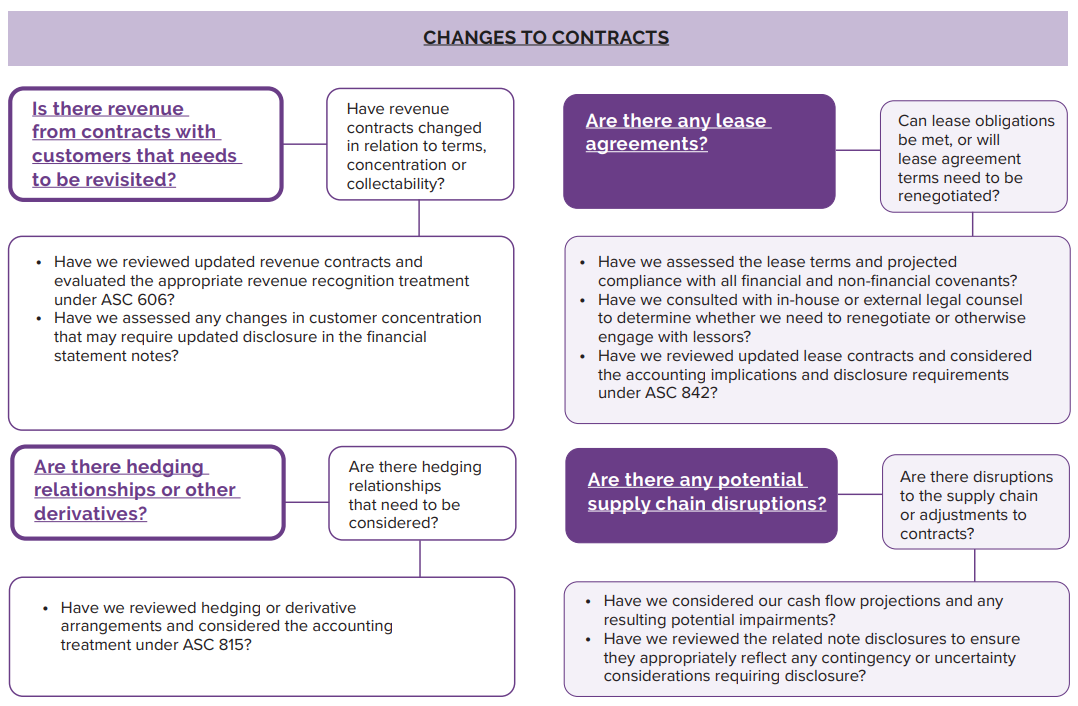

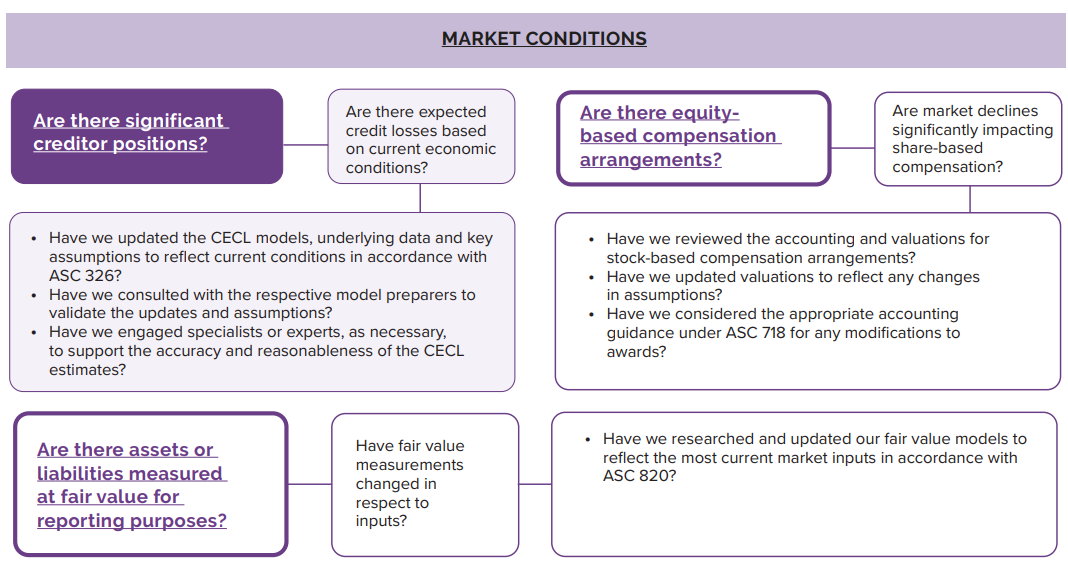

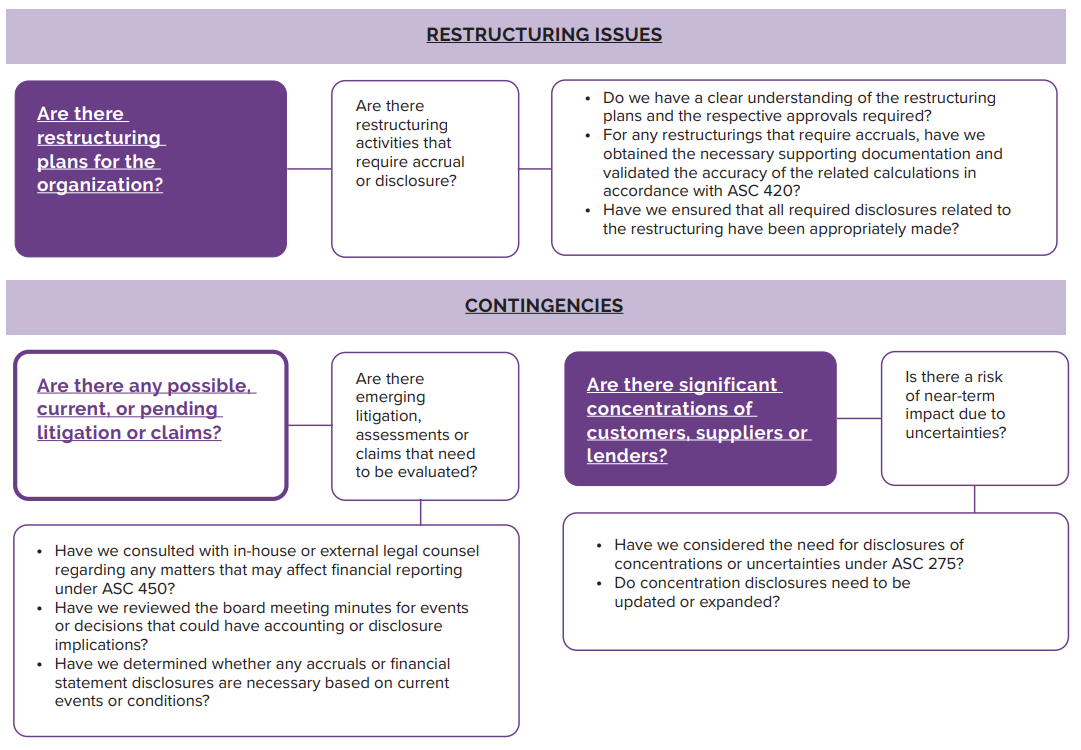

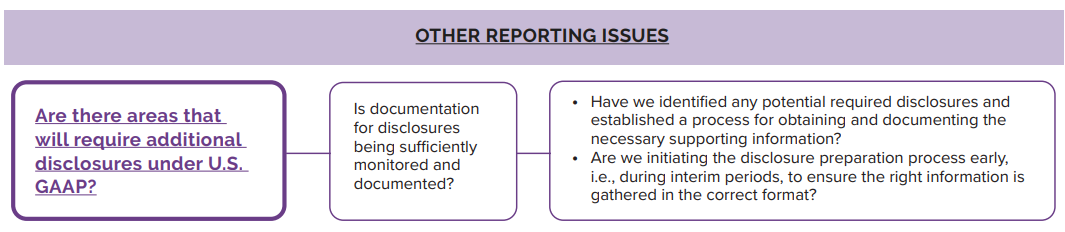

Below are prompts, primary questions and sub-questions that may be asked regarding declining revenue and future cash flows, changes in contracts, market conditions, restructuring issues, contingencies, and other reporting concerns. This table references the relevant areas of U.S. GAAP but does not delve into the specific provisions of each standard. For details and full access to accounting standards, readers should refer to the FASB Accounting Standards Codification (ASC).2

There are potentially many more questions that may be asked that have relevance. Each of these questions, and others, should be addressed through the lens of the appropriate technical accounting guidance related to the entity’s accounting framework (e.g., U.S. GAAP, GASB, IFRS, etc.).

Once appropriate questions have been posed, a key part of the value proposition is starting early, ahead of year-end, to identify what information, resources or inputs are needed to address the issue effectively, such as:

- What is the relevant technical guidance or accounting standard?

- Who needs to be involved or consulted, internally or externally?

- What data is required to research, analyze, and come to a conclusion or to complete computations?

- Are any specialists needed to be engaged in advance? For example, valuation experts, tax consultants, or other advisors. We suggest that periods of uncertainty should not be immediately overwhelmed with efforts to provide answers, but rather, they should be met with questions. Take time to ask questions!

About the Authors

Dr. Amelia Hart, CPA, serves on the faculty of the Haslam College of Business in the Department of Accounting and Information Management at the University of Tennessee, Knoxville. She can be reached at ihart@utk.edu.

Steve Sledge, CPA, is an audit partner at Anglin Reichmann Armstrong. He can be reached at ssledge@anglincpa.com.

References

1Dr. Amelia Hart and Steve Sledge, “Seeing Through the Chaos: An Accountant’s Lens,” Tennessee CPA Journal, Accounting and Auditing Section, May/June 2025.

2For the full authoritative guidance, see FASB Accounting Standards Codification (ASC) https://asc.fasb.org/Home

This article was originally published in the July/August 2025 Tennessee CPA Journal.