By: Josef Rashty, CPA

In March 2024, the SEC adopted its new climate-related disclosure rules (hereinafter, rules) for public business entities (PBEs).1 The rules require a comprehensive discussion of material climate-related risks, identification of climate-related goals, and related greenhouse gas (GHG) emissions. The rules have substantive requirements similar to those in the Task Force on Climate-related Financial Disclosure (TCFD).

The author explored this subject when it was still at its proposal stage in the July/August 2022 Tennessee CPA Journal. The final rules differ in several respects from the SEC’s initial proposal. The most notable are changes to the scope of and number of registrants subject to GHG emission disclosures. This article presents an overview of the SEC’s new promulgation on climate-related and GHG emission disclosures.

Recent Legal Challenges

On March 15, 2024, the U.S. Court of Appeals for the 5th Circuit issued an administrative stay of the SEC’s final rules on climate-related disclosures. This stay introduces uncertainty regarding the future of these disclosure rules, particularly as challenges are also pending in other circuits. These legal hurdles have also forced the SEC to pause its implementation of these requirements. Practically, even if the stay does not remain in place, companies will not need to report under the new rules until 2026 at the earliest.

On March 19, 2024, the Wall Street Journal reported that a coalition of 10 states filed a legal challenge against the new SEC climate-change rules. A 5th U.S. Circuit Court of Appeals granted a request for an administrative stay after several companies filed a legal lawsuit challenging the rules.

Certain oil field services companies filed the petition for the stay, arguing that while the court reviews legal challenges to the new SEC rules, it would be necessary to provide interim relief. The basis for the challenges primarily centers on the argument that the SEC exceeded its authority and that the new rules would impose significant compliance costs on companies.

Scope of SEC’s Promulgation, Severe Weather Events and Greenhouse Gas Emissions (GHG)

The registrants incur losses and recognize them in their income statement (less any insurance recoveries) due to severe weather events and other natural conditions (e.g., hurricanes, tornadoes, flooding, sea level rise) subject to the materiality threshold. The registrants may also incur capitalized costs in their balance sheets (less any insurance recoveries) subject to the materiality threshold.

The SEC rules encompass only the disclosure of climate-related information, which is only one component of sustainability standards. Other standards, such as IFRS Sustainability Disclosure Standards (ISSB Standards) and European Sustainability Reporting Standards (ESRSs), have much broader scope.

There are two different components within the scope of climate-related disclosures:

- Regulation S-X financial statement disclosures that are within the scope of audited financial statements and subject to internal control over financial reporting (ICFR).

- Regulation S-K disclosures in the annual report (Regulation S-K already requires some disclosures). Registrants can include these disclosures in a separate section or incorporate them by reference from another section or another filing.

The SEC does not require greenhouse gas emissions (GHG) disclosures (and early assurance thereon) for all companies. Registrants with Exchange Act reporting obligations under Exchange Act Section 13(a) or Section 15(d) and companies filing a Securities Act registration statement (including foreign private issuers but excluding certain Canadian issuers) are subject to the SEC Rules disclosure requirements.

Climate-related and GHG emissions risks may vary significantly in magnitude and probability over time. Thus, the SEC rules require the registrants to disclose the short-term and long-term risks separately.

The SEC’s Objectives

The SEC always focuses on enhancing and improving the disclosure policies and practices of PBEs rather than mandating them to adopt specific accounting practices. The climate disclosure rules are not different than other SEC promulgations; however, in response to this rule, many registrants may adopt changes to their business and accounting practices.

The SEC’s final rules require disclosures regarding climate-related risks concerning larger registrants and greenhouse gas emissions. The issuers must be mindful that other climate-related disclosures also may apply to them. For example, companies that have business in California or the European Union (EU) should also follow California’s climate disclosure rules or the EU’s Corporate Sustainability Reporting Directive (CSRD).

Greenhouse Gases

Gases that trap heat in the atmosphere are greenhouse gases (GHGs). GHGs occur naturally (e.g., from respiration and decomposition of plants) and cause global warming. Certain human activities may also cause GHG emissions (anthropogenic emissions). Global treaties (such as the Kyoto Protocol and the Paris Agreement) aim to limit global warming to well below 2 degrees Celsius (above pre- industrial level) and pursue efforts to limit it to 1.5 degrees Celsius.

GHGs or greenhouse gases mean carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), nitrogen trifluoride (NF3), hydrofluorocarbons (HFCs), perfluorocarbons (PFCs) and sulfur hexafluoride (SF6). GHG emissions imply direct or indirect emissions

of greenhouse gases expressed in metric tons of carbon dioxide equivalent (CO2e):

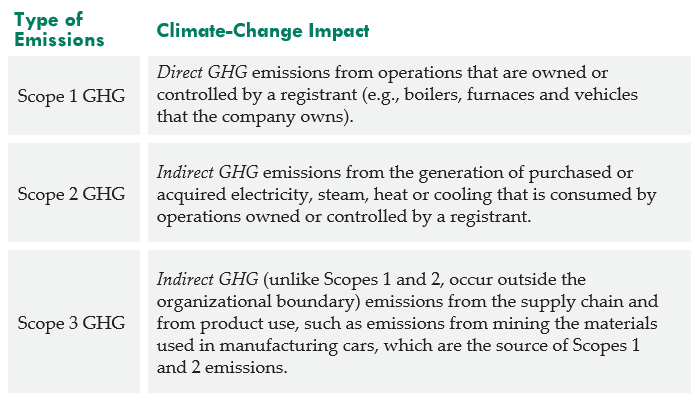

- Scope 1 emissions (direct emissions) are from operations owned and controlled by the registrant.

- Scope 2 emissions (indirect emissions) are from the operations that the registrant consumes but occur at sources that it does not own or control. They are a consequence of downstream divisions related to the use of products and services.

- Scope 3 emissions are consequences of upstream activities, such as purchased goods and services, transportation and distribution, business travel and employee commuting, etc.

GHG emissions reduction at the country level translates to targets at the corporate level. Investors view information on Scopes 1 and 2 GHG emissions as a central measure and indicator of the registrant’s exposure to transition risk as well as a useful tool for assessing its management of transition risk and understanding its progress towards the registrant’s climate-related targets or goals (Item 1505).

The final SEC rules require material GHG emission disclosures for large accelerated filers (LAFs) and accelerated filers (AF) other than the small reporting companies (SRC) or emerging growth companies (EGC). The rules do not prescribe a specific approach for measuring GHG emissions; instead, they require the registrants to disclose their methodologies, significant inputs and assumptions they have used to calculate their GHG emissions.

The most commonly used reference point for the calculation of GHG emissions is the standards and guidance of the GHG Protocol Corporate Standard (GHGP). GHGP is an international set of standards, guidance, tools and training designed to deliver a consistent method of measuring, reporting, and managing GHG emissions.

The earlier SEC proposal that culminated in the final SEC’s promulgation of climate rules on March 6, 2024, envisioned Scope 3 GHG emissions. However, in a reversal from its earlier proposal, the SEC withdrew Scope 3 GHG emissions disclosure requirements. In its final rules, the SEC requires only Scopes 1 and 2 GHG emissions disclosures if material and only for larger companies.

The first step towards emissions reporting is to determine the organizational boundary, which is equivalent to the concept of a “reporting entity” for financial reporting purposes. Once the company determines the organizational boundary, it should determine its operational boundary to determine the direct and indirect GHG emissions.

The earliest compliance date is the fiscal year beginning in calendar year 2025 for large accelerated filers.

Renewable Energy Credits

The SEC refers to “carbon offsets” as “an emissions reduction, removal or avoidance of greenhouse gases (GHGs) in a manner calculated and traced to offset an entity’s GHG emissions” (§229.1500). A GHG offset represents the reduction, removal or avoidance of GHG emissions from a specific GHG project to offset GHG emissions that occur elsewhere.

A company usually sets a GHG emission reduction goal and plan. As the plan progresses, the entity may be required to purchase offset credits to compensate for residual emissions that it cannot eliminate. Renewable Energy Credits (RECs) are tradeable instruments that represent the clean energy attributes (e.g., zero emissions) of renewable energy (e.g., solar, wind, hydropower, geothermal). RECs allow energy buyers to distinguish between renewable and non-renewable energy sources.

Registrants should include disclosure requirements if they use carbon offsets or RECs (Item 1504(d)) as a material component to achieve climate-related goals (the amount of carbon avoidance or carbon reduction).

If RECs are material for the registrants to achieve their climate-related goals (e.g., net-zero commitment), the registrants must disclose a roll-forward of the beginning and ending balances, with separate disclosure of the aggregate amount expensed or capitalized, and the aggregate amounts of related losses incurred at each financial statement line item.

Financial Reporting

The final rules (Item 1502(b)) require the registrant to describe the actual and potential impacts of any climate- related risks identified in response to Item 1502(a) on the registrant’s strategy, business model and outlook.

The final rules require disclosure of capitalized costs, expenditure expenses, charges and losses incurred as a result of severe weather events and other natural disasters. Severe weather events, other natural conditions and controlling GHG emissions can significantly affect public companies’ financial statements in any sector of industries.

These charges also include impairments to the carrying amount of assets (e.g., inventory, intangible assets and property, plant, and equipment) due to their exposure to severe weather, flooding, drought, wildfires, extreme temperatures and the sea level rise. It also includes impairment to goodwill due to a decline in the fair value of the business unit as a result of such expenditures.

However, the final rules also provide small reporting companies (SRCs) and emerging growth companies (EGCs) with a longer phased-in compliance period than other registrants. The final rules, including the amendments to Regulation S-X, will not apply to a private company that is a party to a business combination transaction.

Investors prefer disaggregated disclosures on such expenditures in their income statements and related capitalized costs on their balance sheets.

Materiality Guidance

The SEC rule requires that registrants apply the definition of materiality consistent with the interpretation of materiality set out in the security laws. The SEC deems information material if there is a substantial likelihood that a reasonable investor considers it so. The rules provide the following bright-line guidelines.

The rules require disclosure of expenditures and losses if their aggregate impact is 1% or more of the absolute value of income or loss before taxes for the relevant fiscal year, subject to a $100,000 de minimis threshold.

Companies should also disclose the capitalized costs and expenses if the absolute value of aggregate impact is 1% or more of the value of the stockholder’s equity or deficit at the end of the relevant fiscal year, subject to a $500,000 de minimis threshold.

Registrants should also tag their disclosures for Inline XBRL reporting to help investors and market participants identify, extract, compare and analyze the disclosures.

Attestation

Scopes 1 and 2 GHG emissions are subject to assurance (limited assurance after three years of disclosures and reasonable assurance after four years for large accelerated filers). Final rules (Item 1506(e)) require that any registrant not subject to including a GHG emissions attestation report (under Item 1506(a)) disclose certain information about the assurance engagement if the registrant’s GHG emissions disclosures were voluntarily subjected to assurance. The registrants must also disclose additional information, such as whether they have changed their attestation provider, and if it is subject to oversight inspections. The attestation provider must have significant experience relevant to GHG emissions and be independent of the registrant.

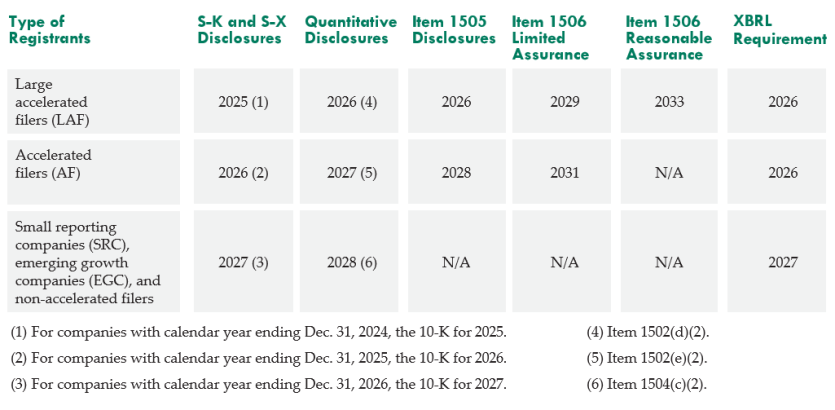

Effective Dates

Fiscal years that appear in the following table imply the beginning of fiscal years. Thus, if a company has a calendar year ending Dec. 31, it files the 10-K for fiscal year 2025 in the first quarter of 2026.

Final Comments

The world of accounting is gradually expanding. We find unfamiliar concepts and terminologies – greenhouse gases and renewable energy – in our profession. Climate-related disclosures are not only a reality for international financial reporting but also in the U.S. since the SEC issued its final rules on climate-related disclosures.

More companies than ever before are facing regulatory requirements to report direct and indirect emissions from their operations. Accountants play a valuable role in bridging the gap between scientific data and information for investors. Thus, it has become more critical for accounting professionals to understand the fundamentals of greenhouse emissions.

The SEC may have dialed back the extent of its new corporate climate disclosure rules, but companies still face challenges in complying with them. Companies had criticized the proposed Scope 3 reporting, and the final rules eliminated the complex and costly

mandate. However, tracking Scope 1 and Scope 2 emission disclosures for the first time will not be effortless for many registrants. The sustainability teams of many companies are not familiar with the level of regulatory scrutiny that financial reporting staff usually adhere to. However, both teams jointly own climate rules reporting and should collaborate in its implementation.

About the Author

Josef Rashty, CPA, Ph.D. (Candidate), provides consulting services in Silicon Valley, California. He is also a faculty and adjunct professor of accounting. He can be reached for comments and suggestions at j_rashty@josefrashty.com.

References

1 SEC Release Nos. 33-11275; 34-00678, The Enhancement and Standardization of Climate-Related Disclosures for Investors.

This article was originally published in the November/December 2024 Tennessee CPA Journal.