By: Dr. Amelia Hart, CPA, and Steve Sledge, CPA

Disclosures are an important and necessary component of financial reports. Disclosures support financial statements with relevant and necessary information. Disclosures are one of the primary means of understanding and explaining the numbers on the face of the financial statements. Given the robustness of our financial reporting ecosystem, there are often competing demands for less and more information from user groups. The FASB continues to seek an appropriate balance when considering requirements for disclosure, which involves evaluating the cost-benefit relationship of certain disclosures, determining what financial information is better expressed via notes versus just numbers, and considering other factors and limitations that could reduce the decision-making usefulness to the users.

On Aug. 28, 2018, the FASB updated the Disclosure Framework. According to the FASB, “the disclosure framework project’s objective and primary focus are to improve the effectiveness of disclosures … facilitating clear communication of the information … that is most important to users.” The framework helps the FASB determine what should be communicated in notes.

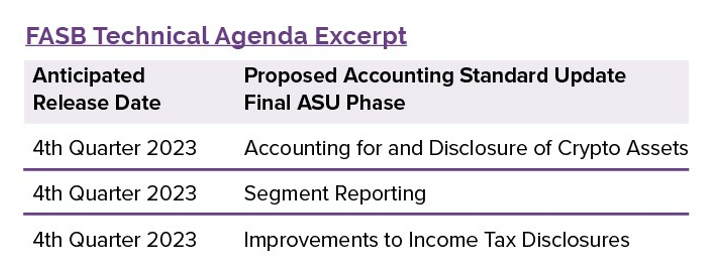

Building on the Tennessee CPA Journal September/October 2023 A&A article covering standards and guidance effective for fiscal year 2023, this article considers the guidance in final phases to be released by the FASB that are disclosure focused. This article provides a summary of the referenced proposed disclosure requirements. Please refer to the final or proposed ASUs for specific guidance and more detailed analysis. The FASB’s Technical Agenda excerpt table indicates the next three ASUs expected to be issued during the fourth quarter of 2023 have disclosure focus. These include Accounting for and Disclosure of Crypto Assets, Segment Reporting, and Improvements to Income Tax Disclosures.

A previous A&A article of the Tennessee CPA Journal (May/June 2023) covered the proposed ASU standard on the disclosure of crypto assets. In lieu of this and in consideration of another potential change in required disclosures, we include an overview of the recent proposed ASU on the disaggregation of Income Statement expense disclosures.

In addition to considering the outlook for the fourth quarter, please also note that the FASB finalized guidance related to joint venture formation. Accounting Standards Update (ASU) 2023-05, issued on Aug. 23, 2023, which relates to Subtopic 805-60 and addresses certain new accounting requirements for joint venture formations.

Currently Proposed ASUs: Focused on Disclosures

While most ASUs have some aspect of guidance related to disclosure requirements as mentioned above, we note that on the FASB’s current technical agenda there are three proposed ASUs with a primary focus on disclosures. Readers are encouraged to review the full proposed standards available at the FASB website.

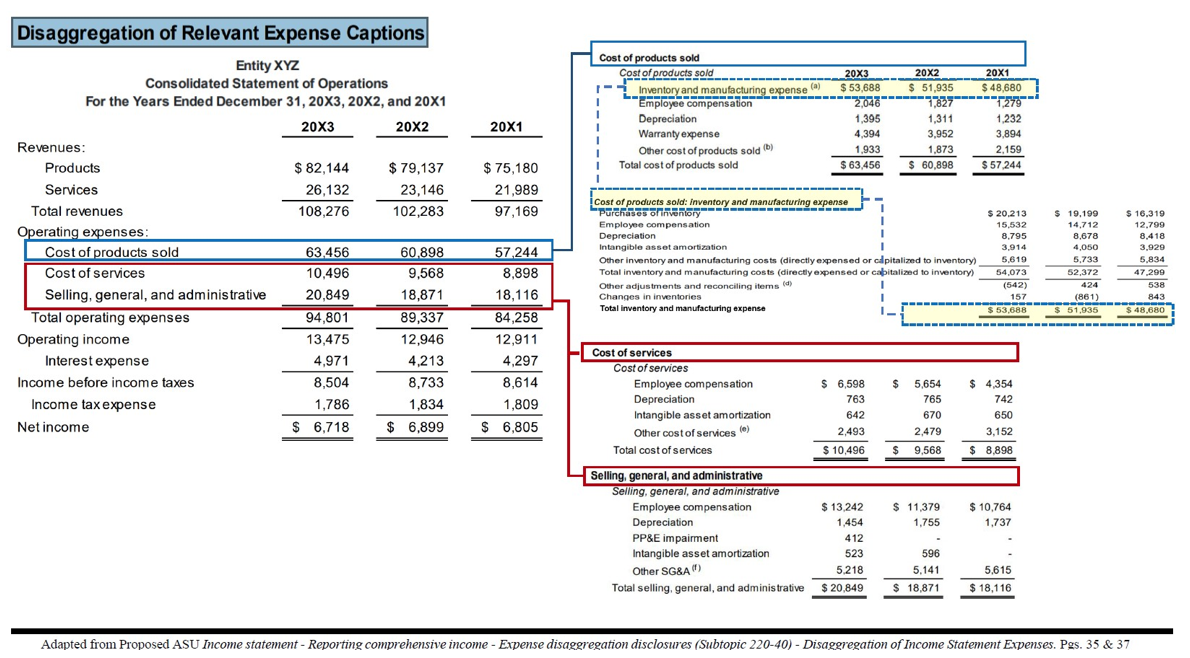

1. Proposed ASU: Disaggregation of Income Statement Expenses [Exposure Draft]

On July 31, 2023, the FASB released a proposed ASU that would impact disclosures of public business entities in the form of an Exposure Draft. The proposed amendment, Income statement - Reporting comprehensive income - Expense disaggregation disclosures (Subtopic 220-40) - Disaggregation of Income Statement Expenses, is in part, a response to investors, creditors, lenders, and other stakeholders’ feedback on the 2021 Invitation to Comment, Agenda Consultation issued by the FASB. The amendment would require public entities to disclose details within categories of certain expense captions, including but not limited to cost of sales and selling, general and administrative expenses. The annual and interim disclosures would show details, if applicable, of:

- inventory and manufacturing expense

- employee compensation

- depreciation

- intangible asset amortization

- depreciation, depletion and amortization expense

Please note that inventory and manufacturing may also be further disaggregated as shown below.

Entities may use a tabular disclosure format for each relevant expense caption and ensure it reconciles to the amount on the face of the income statement. An entity would be required to qualitatively describe the composition of other items that are not required to be disaggregated and is also required to provide its definition of selling expenses and other manufacturing expenses on an annual basis. The proposed amendment is intended to allow for a better understanding of expense items.

EXAMPLE OF DISAGGREGATION OF EXPENSES

2. Proposed ASU: Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures

This proposed ASU is applicable to entities that are required to report segment information under Topic 280 (i.e., public entities) and provides users with greater access to decision-useful information by expanding the scope and frequency of disclosures on reportable segments. This update was also in response to feedback obtained from the FASB’s 2016 Invitation to Comment, Agenda Consultation. The major provisions include the following enhanced disclosure requirements:

- On an annual and interim basis, disclose significant segment expenses regularly provided to the chief operating decision maker (CODM) and included within each reported measure of segment profit or loss. The title and position of the CODM will be required to be disclosed.

- Disclosure of the amount and a description composition of other segment items by reportable segment.

- Disclosure of the reportable segments profit or loss and assets disclosures on an interim basis (currently required on an annual basis by Topic 280).

- Disclosure on whether the CODM applies multiple measures of a segment’s profit or loss, and disclose the measure that is most consistent with principles used by the entity for corresponding amounts in the consolidated financial statements.

- Disclosure of multiple measures of a segment’s profit or loss is permitted, as long as one is the measure most consistent with how the corresponding amounts are measured in the consolidated financial statement.

- Require single reportable segment entities to apply the existing segment disclosures and reconciliation requirements in Topic 280 and those introduced by this proposed ASU.

This proposed ASU is planned for release of a final update in the fourth quarter of 2023. The board has determined that the amendments would be effective for fiscal years beginning after Dec. 15, 2023, and interim periods within fiscal years beginning after Dec. 15, 2024; early adoption would be permitted.

3. Proposed ASU: Income Taxes (Topic 740): Improvements to Income Tax Disclosures

The FASB is seeking to improve the transparency and the usefulness of income tax disclosures in this proposed amendment. Similarly to the proposed amendment on the disaggregation of income statement information, this ASU is a response to feedback from investors, creditors, lenders and other stakeholders on the 2021 Invitation to Comment, Agenda Consultation issued by the FASB. The proposed ASU’s two primary enhancements would (a) disclose specific categories in the rate reconciliation and (b) provide additional information on income taxes paid. The overview below does not provide the scope and depth of the two major requirements. We include a summary for brief insight.

a) Disclosures related to income taxes paid

Per this update, public business entities would use a tabular reconciliation format that shows percentages and amounts of categories specified in the amendment (example, state and local tax, tax credits, valuation allowances, etc.), for reconciling items equal to or greater than a 5% threshold, further broken out by nature and/or jurisdiction. Nonpublic business entities would be required to qualitatively disclose the nature and effect of significant differences between the statutory tax rate in the jurisdiction (country) by specific categories of reconciling items, including other individual jurisdictions

b) Disclosures on certain reconciling items on Income taxes paid

For all entities, the update would require a disclosure in both annual and interim reports of income taxes paid (net of any refunds received) year-to-date, broken out between federal, state and foreign. Entities would also disclose in annual periods the income taxes paid (net of refunds received) to an individual jurisdiction when more than 5% of the total.

The update also removes the burden of certain disclosures for all entities. It would eliminate the need to report on the nature and estimate of reasonably possible changes in the total amount of unrecognized tax benefits expected in the next 12 months of the reporting date and remove the requirement to disclose the cumulative amount of each type of temporary difference when a deferred tax liability is not recognized because of exceptions related to subsidiaries and corporate joint ventures.

The update is intended to promote transparency surrounding rate reconciliation and income taxes paid.

Conclusion

Disclosures are an important and necessary component of the financial reporting ecosystem, and they are a generally accepted accounting principle. The tension that exists between too much versus not enough disclosures will remain a challenge for the standard setters. However, as we continue to prioritize the usefulness of information to decision makers, we can anticipate a heightened level of transparency in financial reporting. General purpose financial statements present one part of the financial story of an entity’s results of operations and financial position; the disclosures facilitate a better understanding of the actions, decisions, outcomes and the possibilities of expected future cash flows.

References

1 The Statement of Financial Accounting Concepts No. 8, Conceptual Framework for Financial Reporting, Chapter 8, Notes to the Financial Statements is available and retrievable at https://bit.ly/3twe2Rt

2 The Tennessee CPA Journal September/October 2023 article, The Standard Setter Has Our Attention: 50 Years Later – FASB Updates Effective Periods Beginning After Dec. 15, 2022 is retrievable at https://bit.ly/3sdrs4n

3 The FASB Technical Agenda provides information about the Boards activity, progress, and milestones at a glance. The full agenda is retrievable at https://bit.ly/fasbtech

4 The Tennessee CPA Journal May/June 2023 article, Prepare for What’s Next: The Proposed Accounting Standard Update on Accounting and Disclosure for Certain Crypto Assets. Article is retrievable at https://bit.ly/tscpaissues

5 The full text of ASU 2023-05 is retrievable at https://bit.ly/3FdQaoc

6 The Financial Accounting Standards Board Updates and Projects are available at https://www.fasb.org/

7 The Exposure Draft, proposed ASU, Income statement - Reporting comprehensive income - Expense disaggregation disclosures (Subtopic 220-40) - Disaggregation of Income Statement Expense is retrievable at https://bit.ly/45sL2ak

8 Per the proposed ASU, the exposure draft defines a relevant expense caption would be an expense caption presented on the face of the income statement within continuing operations including inventory and manufacturing expense, employee compensation, depreciation, intangible asset amortization, and depreciation, depletion, and amortization recognized in oil- and gas-producing activities.

9 The full draft of the proposed Accounting Standards Update, Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures is retrievable at https://bit.ly/topic280

10 The proposed standard is retrievable at https://bit.ly/topic740

About the Authors

Dr. Amelia Hart, CPA, serves on the faculty of the Haslam College of Business in the Department of Accounting and Information Management at the University of Tennessee, Knoxville. She can be reached at ihart@utk.edu.

Steve Sledge, CPA, is a partner at KPMG LLP in Nashville. He can be reached at ssledge@kpmg.com.

This article was originally published in the November/December 2023 Tennessee CPA Journal.